Did you know that besides loans from money lenders and social networks, digital loans are the most frequently used loans in Kenya?

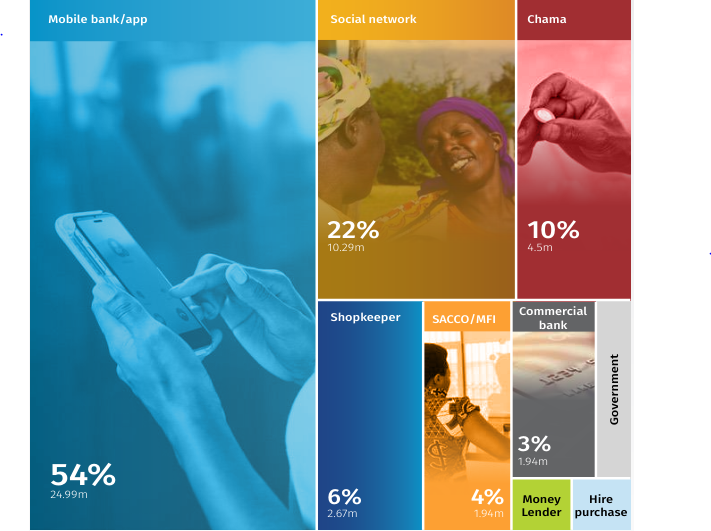

Owing to frequent borrowing, digital loans are the most widely used form of loans, whether official or informal. They make up 54% of the observed market for the average annual loans based on volume.

Average yearly volume of loans disbursed by lenders

The year 2019 saw an estimated KShs 116.8 billion in digital loans given to borrowers or an average of KShs 37,464 per digital borrower annually. After non-digital commercial bank loans and loans from SACCOs and Microfinance institutions, digital loans make up the third-largest source of credit by value, accounting for little less than 9% of the overall observed lending market.

The Average yearly value of loans disbursed by lenders

Who uses digital loans and why?

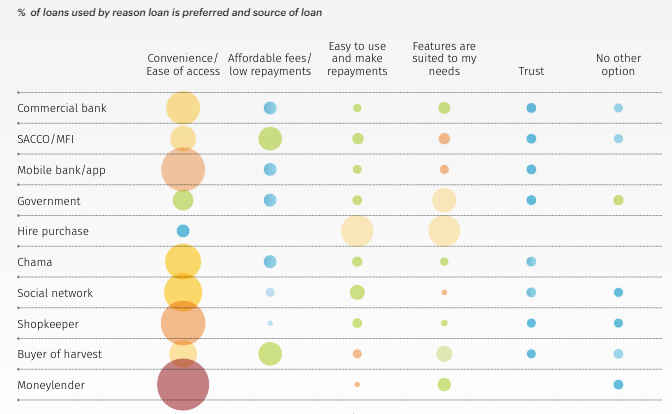

Nearly 2 in 3 digital borrowers report convenience/ease of access as the main reason for choosing digital loans. However, less than 5 percent of digital borrowers report trust as the main reason they borrow digitally compared to the nearly 10 percent of commercial banks, social network or chama borrowers who cite trust as a main reason for borrowing from those sources.

The primary socio-economic and demographic characteristics that set apart digital borrowers from their counterparts are age, place of residence, and income.

Digital borrowers are primarily male (60%) and, in contrast to other formal and even informal borrowers, they are primarily under 35 (62 percent). This is similar to borrowers who utilise formal financial intermediaries such as commercial banks, SACCOs, and Microfinance Institutions.

The concentration of digital borrowers is higher in metropolitan areas: 67% of them reside there, compared to 44% of other formal borrowers and 34% of informal borrowers.

Most borrowers, who are informal, get their income mostly from casual labour or farming (58 percent), whereas, most formal non-digital borrowers (70 percent) get their revenue mostly from employment or farming. However, there is a more even distribution of digital borrowers across livelihood categories: the largest category (29 percent) is made up mostly of self-employed people, slightly more so than employed people (27 percent).

Digital borrowers fall somewhere in the centre of the income distribution between solely informal borrowers, who are mostly at the lower end, and formal (non-digital) borrowers, who are primarily at the upper end. Compared to KShs 7,705 for only informal borrowers and KShs 28,608 for other formal borrowers, the average self-reported monthly income of digital borrowers is KShs 20,120.

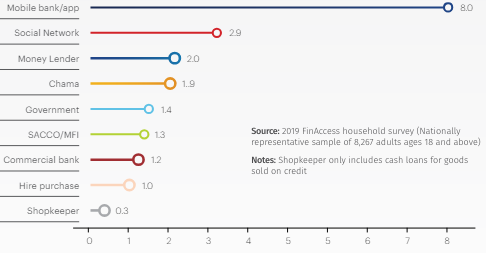

Frequency of borrowing by customers as per the categories of lenders

Average number of loans per person taken every 12 months, by source of loan.

Source: 2019 FinAccess Household Survey

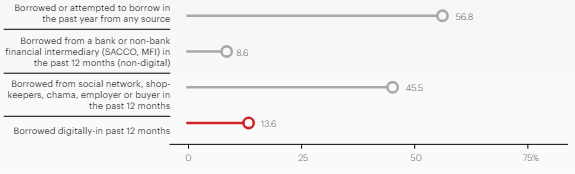

The latest FinAccess survey in 2019 found that 13.6 percent of adults (18+) nationally (3.42 million adults) had used a digital (mobile banking or app) loan in the year prior to the interview. To put this into context, consider that 9 percent of adults reported using a traditional loan from a bank or non-bank financial intermediary and 45 percent of adults reported using a loan from informal sources such as friends or community savings groups.

The need for credit is high and is mainly supplied via unofficial means, although digital credit accounts for a sizable portion of that demand.

How have Telecommunication giants such as Safaricom impacted the digital lending space?

M-Shwari accounts for 34% of Kenya’s local digital lending sector, closely followed by Fuliza at 25%, followed by KCB M-Pesa at 12%.

Kenya has experienced massive digital credit lending services growth since the launch of M-Shwari in 2012.

Digital lending apps have additionally been fueled by increased food prices and unemployment rates, forcing citizens to run to almost anything that can put food on their table. Currently, the country boasts 51 digital credit providers.

The State of Digital Lending Report 2021 released by Reel Analytics, showed that 55 of every 100 people acquire loans from digital lending applications.

The study revealed that digital lending platforms were more popular in urban areas (66%) compared to rural areas (34%).

The data indicated that 59% of men had used digital lending platforms and had multiple digital credit providers compared to women who preferred a single brand.

“Most users of digital credit subscribers are aged between 30-34 years, constituting 26% and 22% of male and female beneficiaries, respectively.

Most Kenyans prefer digital lending platforms due to convenience, easy access, and fast loan remittance,” the report stated.

The survey found that 35% of Kenyan Digital Credit borrowers do so to meet day-to-day household needs, while 37% borrow for business reasons.

Percentage of adults who used a loan in the year, 2018 by source of loan